A Red Card for Puerto Rico Tax Incentives?

Peter Palsen, International Tax Professional

In the 2018 book Red Card – How the U.S. Blew the Whistle on the World’s Biggest Sports Scandal, author Ken Bensinger spends 368 pages discussing how the Internal Revenue Services (IRS), Treasury Financial Crimes Enforcement Network (FinCEN) and the Federal Bureau of Investigation (FBI) collectively carried out a cross-border, financially-related, criminal investigation. Part of that investigation involved obtaining indictments of lower-level participants and turning them into information access and testimony favorable to the government case. A recent development suggests that a similar effort may be underway in connection with the use of Puerto Rico and U.S. tax incentives.

Do you need help with the U.S. tax aspects of your

Puerto Rico arrangements?

Contact our tax team at (410) 497-5947 or fill out our brief contact form.

An indictment filed October 14, 2020 alleges that a senior tax partner (Defendant) of a large public accounting firm in Puerto Rico, along with “others known and unknown…devised and intended to devise a scheme and artifice to defraud the Internal Revenue Service…” The indictment describes an IRS sting operation wherein an undercover IRS-CI special agent posed as a wealthy U.S. taxpayer seeking to evade taxes by exploiting the Puerto Rico tax incentives.

Allegedly, Defendant formed a company under Puerto Rico law for the undercover agent in furtherance of such goal. Moreover, the indictment alleges the accused parties’ unjust enrichment by their acceptance of fees for false and fraudulent acts. Significantly, and more specifically, the accused are alleged to have prepared and filed (and caused to be filed) tax incentive applications and Puerto Rico and U.S. tax returns. According to a press release issued by the U.S. Department of Justice, the senior partner was arrested by federal law enforcement officers from the IRS criminal investigation unit.

The indictment makes clear that the subject matter of the “scheme” involves the tax incentives afforded to businesses and individuals under Acts 20 and 22 of Puerto Rico law.1 In short, Act 20 allows a Puerto Rican corporation to pay tax at a federal rate of 4% on qualified export sales and also provides for an exemption on dividends of the earnings. Act 22 provides individual tax exemptions for passive types of income. These provisions have been in place since 2012, and thousands of U.S. citizens have been reported to have availed themselves of the benefits of the provisions to obtain a low Puerto Rican tax rate.

The reason that these exemptions are interesting for U.S. citizens is a result of the fact that the U.S. is one of few countries that taxes its citizens on worldwide income—so moving outside of the United States while retaining U.S. citizenship does not generally reduce U.S. taxes. However, in the case of U.S. citizens taking up bona-fide residence in Puerto Rico, Internal Revenue Code (IRC) §933 can allow them to exempt from U.S. tax certain income that has its source in Puerto Rico.

Section 933 was not designed as an incentive for U.S. citizens trying to enjoy the benefits of Acts 20 and 22 (which are generally not available to ordinary Puerto Rican residents), but rather a mechanism to effectively allow Puerto Rico to apply its country tax laws to raise revenue (and provide benefits from such revenue) to its residents. To illustrate, a doctor or taxi driver living and working in Puerto Rico will pay taxes to the Puerto Rico government. As long as all of their income is earned in Puerto Rico, IRC §933 relieves them of their obligation (as U.S. citizens) to also pay income tax in the U.S.

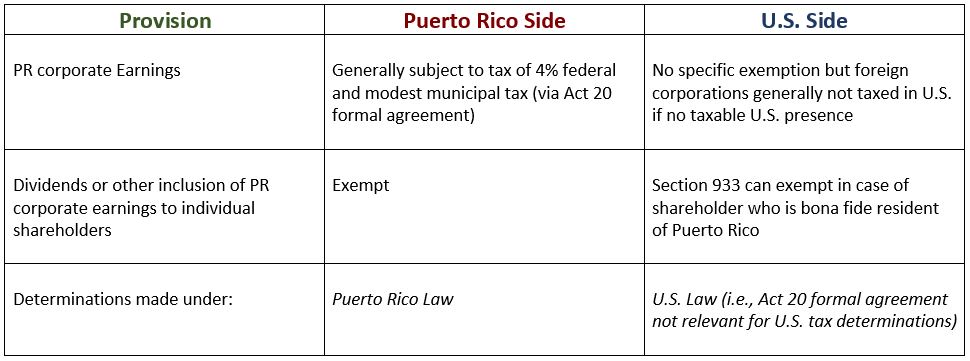

A short matrix will provide the context for further discussion of the “scheme”:

As noted in the matrix, United States tax law provides no specific incentives related to the taxation of Puerto Rican companies, which are treated as foreign corporations under U.S. tax law. However, to the extent that a foreign corporation (from any country) does not have a U.S. taxable presence (directly or through certain agents), it can avoid direct federal taxation in the United States.

The specific U.S. tax incentive related to a Puerto Rico company applies when the earnings of such a company (i.e., dividends or accelerated U.S. tax inclusions) are treated as Puerto Rican source income that can be exempt from U.S. federal tax (under IRC §933). In order to qualify for this exemption, an individual shareholder must be treated as a resident in Puerto Rico under stringent “bona-fide” resident tests applied under U.S. tax law. In other words, if a U.S. citizen moves to Puerto Rico and establishes behaviors of residency similar to the doctor or taxi-driver, he or she can also claim the benefits of the exemption.

The “scheme” at the center of the indictment involved the establishment of a Puerto Rican company that applied for (and presumably received) the benefits of Act 20. The Puerto Rican company would logically be intended to not have a U.S. tax presence so it could avoid direct U.S. taxation. It should be noted here that the use of an offshore company to provide services to a related U.S. company is a widely used and well-established concept in international taxation. There are many such companies in operation that receive service fees from U.S. companies and do not pay direct U.S. tax.

To the extent there is controversy with respect to the use of a related-party offshore service company, it typically involves an argument about a fair market-rate payment for the services provided. According to the indictment, a figure of $500,000 was established for the services, and such amount was intended to be invoiced to a U.S. company and deducted as a business expense – thus providing a U.S. tax benefit. It is unclear how the service fee was determined, but if the underlying services were illusory, logically any figure would be viewed as excessive under the circumstances.

To carry the “scheme” to its operational conclusion, the earnings of the company (the $500,000 less any deductible expenses) could have been distributed tax-free in Puerto Rico and, by implication of the information in the indictment, would have avoided U.S. tax via IRC §933.

How should beneficiaries of Act 20 and Act 22 feel about this development?

First off, to the extent actual services had been provided (and properly priced) and bona-fide residence established for the shareholder to qualify under IRC §933, the intended results would not appear to be egregious. Put another way, the underlying arrangements (if valid) would not constitute an obvious tackle from behind.

But the red card is out. The U.S. government has conducted a multi-year criminal investigation which on its surface involves the avoidance of $150,000 of U.S. tax. There are others— “known and unknown”—who will apparently be pursued. In this regard, beneficiaries of Act 20 and Act 22 might want to settle down with a good book and wait for further developments.

The indictment makes clear that the subject matter of the “scheme” involves the tax incentives afforded to businesses and individuals under Acts 20 and 22 of Puerto Rico law.1

If you would like to review the U.S. tax aspects of your Puerto Rico arrangements or have other questions about international tax structuring or controversy, then schedule a consultation or call our team at(410) 497-5947.

1“For more information regarding these Acts, see our previous post Tax-Weary Americans Find Haven in Puerto Rico.